It’s critical to do your homework before entering a relationship. You wouldn’t marry someone without getting to know them first, and you wouldn’t hire someone without doing an interview first. Why take the risk of creating a poor relationship with a new client or customer?

Know Your Customer (KYC) is a procedure that allows businesses to verify that their customers are who they say they are. This is often done in two stages: during the onboarding of new clients and on a regular basis for existing customers. The goal is to have a robust KYC and due diligence procedure in place in order to limit the risk of money laundering in your financial system.

The following are examples of typical KYC controls:

Program for customer identification

Documents of identification

Identification of any previously identified parties

Transactions of Politically Exposed Persons (PEPs)

KYC Documents Must Be Provided

Individuals and companies both go through the KYC process. KYC authentication is based on the verification of an individual’s identity and address. The documents necessary for the KYC procedure for individuals include the standard paperwork that people use, such as:

Driver’s license

Social security card/number

Passport

Documents issued by the state or the federal government.

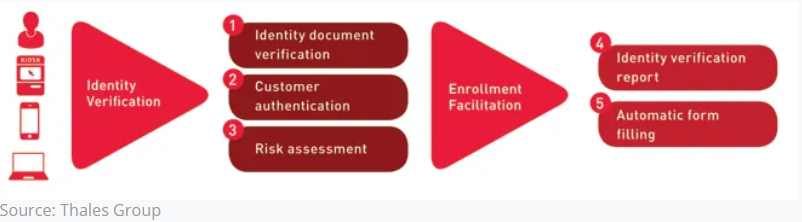

KYC (Know Your Customer) Process

The KYC procedure is straightforward and varies very little from one jurisdiction to the next. The following is a diagram of a basic KYC process flow:

Step 1: Documents must be submitted

An application for financial services or a potential user of financial services must present documentation to verify their identification and residency status. The submission can be made in either electronic or paper format.

Step 2: Verify your identity

Based on the document presented and valid identification, the authorized agency/organization conducts identity verification. If the applicant produces a driver’s license, for example, the Land Transportation Office will conduct the verification

Step 3: Verification of residency

The residency verification process necessitates determining the resident status (domestic or foreign), current residential address, alternate residential address, citizenship status, and other factors.

Step 4: Checking your financial situation

Documents, phone calls to the issuer, and physical checks are used to verify the assets and obligations claimed. This lowers the likelihood of falsification.

Step 5: Transactions monitoring

The financial institution examines the customer’s/transactions, client’s and any transaction that is unusual/high-valued, frequent, or otherwise unusual is flagged automatically and subjected to manual scrutiny.

Know Your Clients(KYC) assists organizations such money remittance centers and commercial banks among others in understanding and managing potential risks during the customer onboarding process, in addition to preventing criminal exploitation. As a result, businesses may appear more trustworthy to potential new clients.

The following are some of the most significant challenges:

- Businesses must undertake KYC validation tests on a regular basis in order to upgrade or downgrade consumer risk profiles. This is frequently done manually, which is not only time consuming but also potentially dangerous in terms of operational and regulatory hazards.

- Making KYC adjustments, uploading documentation, and making partial withdrawals are all made simple as part of reaching out to clients. In some circumstances, changing contact information such as email address, phone number, and correspondence address is done online without verification. There is a danger of disbursement without sufficient identification of the transacting parties as a result of this. As a result, KYC verification is required prior to any disbursement.

- Frequently, high risk businesses that handle numerous lines of business (bank accounts, life and general insurance, and remittances) would request KYC documents from the same consumer many times, resulting in KYC processing duplication. To centralize the KYC process, data must be reconciled across enterprises.

Importance of Know Your Client(KYC)

Establishes the customer’s honesty and sincerity

Banks and other financial institutions work with a wide variety of individuals. When dealing with sensitive financial matters, institutions must prove the legitimacy of these people’s identities, whether they are individuals or businesses. KYC aids businesses in obtaining sufficient proof for the same purpose.

It makes it easier to keep track of transactions

KYC assists financial institutions in avoiding transactions with corrupt individuals or groups, politically exposed persons (PEPs), and those with criminal motivations such as terrorism financing, drug trafficking activities, laundering activity and fraud. Financial institutions can ensure that their services are not exploited by adhering to KYC guidelines correctly.Is a vital risk-reduction strategy

The KYC system considerably minimizes the risk of money laundering, theft, and other monetary dishonest acts in a sensitive and crucial industry like banking and financial services since it identifies businesses with questionable backgrounds early on.After acquiring and certifying this data, financial institutions send it to the Anti Money Laundering Council (AMLC). The same data is entered into a central database by AMLC. In the event that the information changes in the future, only the appropriate piece is updated.

Know your Client(KYC) Benefits

Onboarding processes have been completely improved and digitized thanks to the most advanced artificial intelligence technologies, removing any friction and making it easier for users to access remote contracting of products and services in a completely secure manner, not only in banking but across all industries.

In their platforms, not all Know Your Customer service providers use the most up-to-date methodologies and tools. As a result, relying on comprehensive KYC solutions that assist both the company and the user during the onboarding process, as well as subsequent authentication needs, while offering the highest regulatory and technological assurances, is crucial.

Otherwise, it’s very likely that the solution will not be fully compliant with current standards and will not provide all of the benefits that incorporating this technique should provide. It is impossible to stress the importance of focusing on the user experience and following a quality procedure.

Asynchronous Video IDentification is now feasible in a matter of seconds, from any device and across any channel. Acquiring a customer has never been easier, thanks to the most stringent global regulations (AML5, eIDAS).

The different technologies available for digital identification and existing KYC solutions are generating a lot of noise in the market. As a result, having a qualified reference partner for any Know Your Customer needs that the firm may have is critical.

Additional benefits:

- Delivery at a low cost

- Advancement towards a digital organisation

- Systems that are both secure and scalable

- Customer onboarding is improved

- Humans are exposed to less sensitive info.

- Customer satisfaction has improved

Final Thoughts

Know Your Customer policies are an effective technique of lowering the risk of fraud while simultaneously satisfying a business’s need to know who the user actually is as a compliance concern. KYC allows businesses to protect themselves by ensuring that they are transacting business with legal entities. It also safeguards people who could otherwise become victims of financial crime.

Additionally, technological innovation in the financial sector in the client identification process has become a priority due to the numerous benefits it delivers, including reduced paper consumption, increased data precision, and improved customer service, all while maintaining real-time compliance.

References:

VIKASPEDIA

COINMETRO

AMLC

BROWNEDU

BISORG

COINMETRO

NEWBANKING

PYMNTS

COMARCH

CORPORATEFINANCEINSTITUTE

JUMIO